In 2022, global inflation soared due to the pandemic aftermath and geopolitical events, challenging central banks' targets. An unexpected surge in bond yields added to uncertainty, impacting Argentina's fragile economic stability. Argentina's elections were marked by inflation concerns and a proposal to adopt the US dollar as the national currency. The election's first round intensified market suspense, with an inconclusive outcome. As Argentina teeters on the brink of change, the world awaits the second round, holding the key to the nation's future. The suspenseful narrative of Argentina's economic and political fate remains open-ended, with the world anxiously anticipating the next chapter.

Macroeconomic Outlook on Inflation and Policy Rates

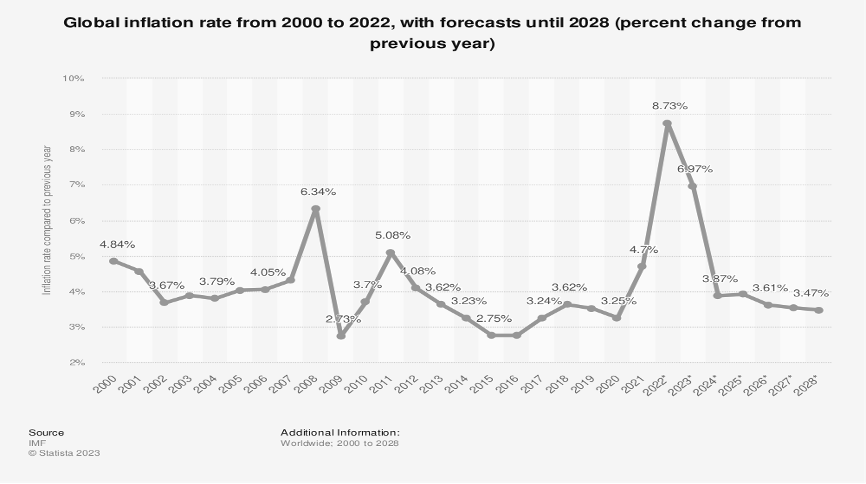

In the aftermath of the COVID-19 pandemic and Russia's incursion into Ukraine, global inflation soared to multi-decade highs in 2022. These inflation levels significantly exceeded the targets set by central banks, particularly in advanced economies.

In the aftermath of the COVID-19 pandemic and Russia's incursion into Ukraine, global inflation soared to multi-decade highs in 2022. These inflation levels significantly exceeded the targets set by central banks, particularly in advanced economies.

As policy measures gradually recalibrate aggregate demand towards potential output, disruptions in supply chains have subsided, and commodity prices have receded. Consequently, headline inflation is on a downward trajectory. However, underlying price pressures, as indicated by core inflation, continue to remain elevated.

Notably, professional forecasters anticipate that inflation rates will approach central banks' targets once again by 2024. This will entail a shift in their median deviation towards zero, along with a pronounced narrowing of the distribution. However, it is also their expectation that, given the current contractionary stance and the anticipated policy actions in the foreseeable future, inflation rates will only fully return to their targets by 2026, on average.

In both advanced and emerging market economies, various indicators of inflation expectations, including the average absolute deviations from the target, the variability of expectations over time, and the degree of disagreement among individuals, collectively suggest that long-term inflation expectations have remained firmly anchored, despite recent increases in inflation. This consistency is reassuring, but it should not be taken for granted. It likely reflects, at least in part, the proactive efforts of policymakers to mitigate upward pressure on prices.

Present trends in actual inflation broadly align with historical medians, although near-term inflation expectations exhibited a more pronounced ascent and a swifter decline compared to earlier episodes. After a year of persistently rising inflation expectations, economies typically witness a gradual but slow decline in headline inflation and short-term inflation expectations.

Notably, professional forecasters anticipate that inflation rates will approach central banks' targets once again by 2024. This will entail a shift in their median deviation towards zero, along with a pronounced narrowing of the distribution. However, it is also their expectation that, given the current contractionary stance and the anticipated policy actions in the foreseeable future, inflation rates will only fully return to their targets by 2026, on average.

In both advanced and emerging market economies, various indicators of inflation expectations, including the average absolute deviations from the target, the variability of expectations over time, and the degree of disagreement among individuals, collectively suggest that long-term inflation expectations have remained firmly anchored, despite recent increases in inflation. This consistency is reassuring, but it should not be taken for granted. It likely reflects, at least in part, the proactive efforts of policymakers to mitigate upward pressure on prices.

Present trends in actual inflation broadly align with historical medians, although near-term inflation expectations exhibited a more pronounced ascent and a swifter decline compared to earlier episodes. After a year of persistently rising inflation expectations, economies typically witness a gradual but slow decline in headline inflation and short-term inflation expectations.

Bonds Market

At the start of this year, market analysts and investors were anticipating a different scenario in the world of bonds. The prevailing expectation was that bond yields would be heading lower as 2023 progressed. Instead, the bond market has witnessed a sharp rise in yields, with long-term U.S. Treasury bonds hitting their highest levels since October 2007. The 10-year U.S. Treasury note reached a recent high of 4.83%, a significant increase from 4.09% at the end of August and 3.79% at the beginning of the year. This unexpected surge in bond yields has raised questions about the factors behind this trend and its potential implications.

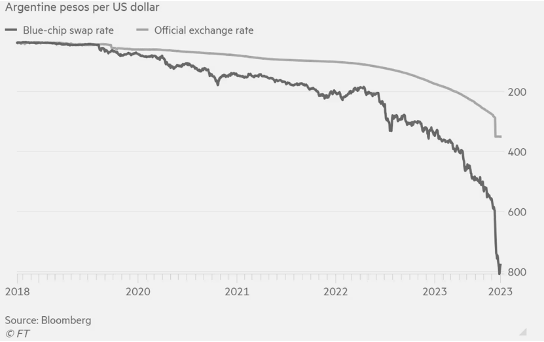

This surge in bond yields coincides with a growing concern among international investors regarding Argentina's economic future. Amidst this political and economic turmoil, investors are apprehensive about Argentina's prospects in the lead-up to November. The devaluation of the exchange rate is exacerbating the country's already severe inflation problem, potentially leading to hyperinflation. The aftermath of Milei's primary election victory saw the price of Argentine dollar bonds plummet by as much as 15%, and the peso weakened on unofficial exchange rates. The central bank responded by devaluing the official exchange rate to 350 pesos per dollar. The blue-chip swap rate, an indicator for international investors, has continued to weaken, surpassing 780 pesos to the dollar on Friday. These developments underscore the significant challenges and uncertainties facing Argentina's economic and political landscape in the coming months

At the start of this year, market analysts and investors were anticipating a different scenario in the world of bonds. The prevailing expectation was that bond yields would be heading lower as 2023 progressed. Instead, the bond market has witnessed a sharp rise in yields, with long-term U.S. Treasury bonds hitting their highest levels since October 2007. The 10-year U.S. Treasury note reached a recent high of 4.83%, a significant increase from 4.09% at the end of August and 3.79% at the beginning of the year. This unexpected surge in bond yields has raised questions about the factors behind this trend and its potential implications.

This surge in bond yields coincides with a growing concern among international investors regarding Argentina's economic future. Amidst this political and economic turmoil, investors are apprehensive about Argentina's prospects in the lead-up to November. The devaluation of the exchange rate is exacerbating the country's already severe inflation problem, potentially leading to hyperinflation. The aftermath of Milei's primary election victory saw the price of Argentine dollar bonds plummet by as much as 15%, and the peso weakened on unofficial exchange rates. The central bank responded by devaluing the official exchange rate to 350 pesos per dollar. The blue-chip swap rate, an indicator for international investors, has continued to weaken, surpassing 780 pesos to the dollar on Friday. These developments underscore the significant challenges and uncertainties facing Argentina's economic and political landscape in the coming months

The unexpected surge in bond yields has important implications for various market segments. Here are some key takeaways:

1. Inverse Yield Curve Concerns: The surge in long-term yields has lessened the degree to which short-term yields are higher than long-term yields, known as an inverted yield curve. Historically, this phenomenon has been considered a precursor to a recession. However, recent trends suggest a reversal of this dynamic, with long-term yields rising while short-term rates remain stable.

2. Investor Caution: The rise in bond yields has led to a cautious stance among investors. While higher long-term rates might appear attractive, there is hesitancy due to the need for high confidence in the economy's performance, given the current strength of the job market and the risk of reigniting inflation.

3. Federal Reserve Influence: The Federal Reserve's decisions and communication are expected to play a pivotal role in shaping the future of bond yields. As the central bank balances the need to support economic growth with concerns about inflation, its actions will be closely monitored by market participants.

1. Inverse Yield Curve Concerns: The surge in long-term yields has lessened the degree to which short-term yields are higher than long-term yields, known as an inverted yield curve. Historically, this phenomenon has been considered a precursor to a recession. However, recent trends suggest a reversal of this dynamic, with long-term yields rising while short-term rates remain stable.

2. Investor Caution: The rise in bond yields has led to a cautious stance among investors. While higher long-term rates might appear attractive, there is hesitancy due to the need for high confidence in the economy's performance, given the current strength of the job market and the risk of reigniting inflation.

3. Federal Reserve Influence: The Federal Reserve's decisions and communication are expected to play a pivotal role in shaping the future of bond yields. As the central bank balances the need to support economic growth with concerns about inflation, its actions will be closely monitored by market participants.

China-Argentina SWAP Deal

In the complex realm of international finance, bilateral currency swap agreements often play a pivotal role in stabilizing economies and fostering economic cooperation between nations. One such agreement of significant importance is the China-Argentina currency swap deal. This renewed agreement, valued at 130 billion yuan (approximately 4.5 trillion Argentine pesos or $18.2 billion), carries far-reaching implications for both countries and their economic landscapes. In this section, we delve into the details of the China-Argentina currency swap deal, exploring its motivations, potential outcomes, and broader implications.

Argentina currently finds itself grappling with a severe shortage of foreign exchange reserves in U.S. dollars, coupled with an inflation rate exceeding 100 percent. This economic predicament has posed substantial challenges for the Argentine government and its efforts to stabilize the country's financial situation. In light of these challenges, the renewal of the currency swap agreement between China and Argentina is viewed as a strategic move aimed at providing much-needed support to the beleaguered Argentine peso and alleviating the economic challenges the country faces. Simultaneously, the renewal of the China-Argentina currency swap deal deepens the economic and trade cooperation between the two nations.

Moreover, in June, China and Argentina signed a cooperation plan in Beijing, aimed at jointly advancing the construction of the Belt and Road Initiative. This plan underscores their commitment to deepening bilateral economic and trade collaboration. China's leading economic planner has also highlighted plans to enhance cooperation in infrastructure, energy, economy and trade, finance, and people-to-people and cultural exchanges.

This renewed agreement follows the expansion of the currency swap deal between China and Argentina earlier this year. Furthermore, central bank governors from both nations have committed to further enhancing the use of the yuan in the Argentine market. The first currency swap agreement between China and Argentina was initially signed in 2009, amounting to 70 billion yuan, and it was valid for three years. In July 2017, China's central bank renewed the swap agreement with the Central Bank of Argentina, allowing for the exchange of 70 billion yuan for 175 billion Argentine pesos. Subsequently, in December 2018, a supplementary swap deal for 60 billion yuan was signed, building upon the agreement inked in July 2017. The expansion of the Argentina-China currency swap deal is a vital step in addressing Argentina’s economic woes, offering a lifeline in the face of rising bond yields. However, the outcome of the general election will determine how effectively this partnership can steer Argentina toward a macroeconomic stability.

In the complex realm of international finance, bilateral currency swap agreements often play a pivotal role in stabilizing economies and fostering economic cooperation between nations. One such agreement of significant importance is the China-Argentina currency swap deal. This renewed agreement, valued at 130 billion yuan (approximately 4.5 trillion Argentine pesos or $18.2 billion), carries far-reaching implications for both countries and their economic landscapes. In this section, we delve into the details of the China-Argentina currency swap deal, exploring its motivations, potential outcomes, and broader implications.

Argentina currently finds itself grappling with a severe shortage of foreign exchange reserves in U.S. dollars, coupled with an inflation rate exceeding 100 percent. This economic predicament has posed substantial challenges for the Argentine government and its efforts to stabilize the country's financial situation. In light of these challenges, the renewal of the currency swap agreement between China and Argentina is viewed as a strategic move aimed at providing much-needed support to the beleaguered Argentine peso and alleviating the economic challenges the country faces. Simultaneously, the renewal of the China-Argentina currency swap deal deepens the economic and trade cooperation between the two nations.

Moreover, in June, China and Argentina signed a cooperation plan in Beijing, aimed at jointly advancing the construction of the Belt and Road Initiative. This plan underscores their commitment to deepening bilateral economic and trade collaboration. China's leading economic planner has also highlighted plans to enhance cooperation in infrastructure, energy, economy and trade, finance, and people-to-people and cultural exchanges.

This renewed agreement follows the expansion of the currency swap deal between China and Argentina earlier this year. Furthermore, central bank governors from both nations have committed to further enhancing the use of the yuan in the Argentine market. The first currency swap agreement between China and Argentina was initially signed in 2009, amounting to 70 billion yuan, and it was valid for three years. In July 2017, China's central bank renewed the swap agreement with the Central Bank of Argentina, allowing for the exchange of 70 billion yuan for 175 billion Argentine pesos. Subsequently, in December 2018, a supplementary swap deal for 60 billion yuan was signed, building upon the agreement inked in July 2017. The expansion of the Argentina-China currency swap deal is a vital step in addressing Argentina’s economic woes, offering a lifeline in the face of rising bond yields. However, the outcome of the general election will determine how effectively this partnership can steer Argentina toward a macroeconomic stability.

Economic outlook and challenges after elections

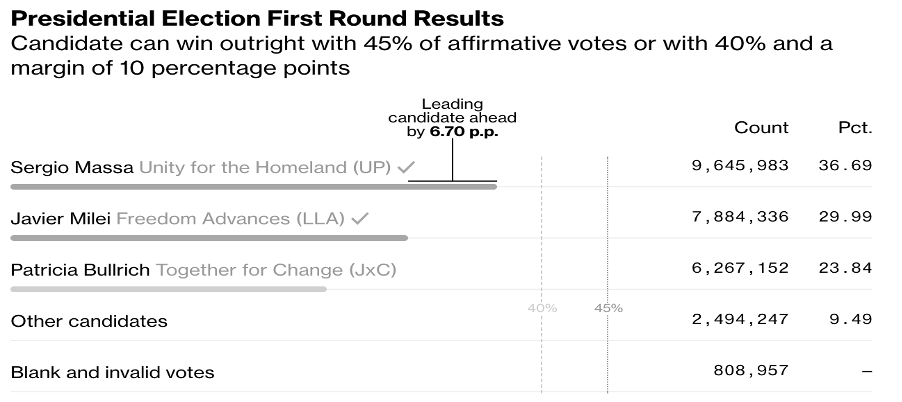

On October 22, Argentinians headed to the polls to cast their votes in the first-round general election to determine the country’s next president. To secure the win in the presidential elections within the first round, the leading candidate must have 45% of the votes or 40% of votes with a 10%-point lead with the second candidate. The implications of the election are profound for Argentina’s economic prospects.

According to a Poll conducted by CEOP Latam, a market research firm, when voters were asked what their greatest concerns were about the new election, 82.2 percent of the respondents chose “the economy and inflation” as the major concern for the current elections. Indeed, October’s Inflation rate hit 138.30%, the highest inflation rate since 1991, and with the central bank publishing forecast for inflation to reach 169.3%, the situation is more likely to get worse before showing signs of improvement.

Meanwhile, the ruling Peronist coalition has tried to boost its electoral chances by announcing that it will give two payments to informal workers, representing around half of Argentina’s labor force, totaling about 270$. The payouts will be financed by imposing extraordinary taxes on banks and on other big corporation who benefitted the most from the devaluation of peso in august, a measure that was part of the 44-billion financing program for the country made by the International Monetary Fund. This measure was implemented after the Mandatory Open Primaries election result, with the central bank rising the interest rate from 97 percent to 118 percent to weaken the currency to 350 Argentine pesos per dollar.

Currently leading the Runoff that will take the electors to cast their final vote on the 19th of November are Javier Milei, a libertarian from the Liberty Advances Coalition and Sergio Massa, National deputy for the centre-left coalition “Frente de Todos”

The most notable measure in Milei’s plan is to abandon the peso, shutdown the central bank and adopt the dollar as Argentina’s national currency. This maneuver was proposed with the argument that there is no price stability, and the independence of the central bank is just an illusion. Some citizens have already been preparing for a dollarization scenario by trying to acquire as much of the US currency as possible.

One of the main problems faced by Argentina is in fact the currency muddle caused by a multitude of dollar exchange. The government keeps control over the value of the currency by preventing the purchase of foreign exchange to protect its decreasing reserve. The Over-protecting behavior has led to the rise of an informal market for the dollar such that the parallel currency is now at three times the value of the official rate. This disparity has led the way for lots of alternative exchanges, such as the “Coldplay Dollar” for concert tickets or “Soy Dollar” for the agriculture sector.

Argentines convert their cash to dollars on the black market, and the Central bank estimates about 244$ billion is stashed away in homes, which is the ultimate signal of distrust in the peso.

On October 22, Argentinians headed to the polls to cast their votes in the first-round general election to determine the country’s next president. To secure the win in the presidential elections within the first round, the leading candidate must have 45% of the votes or 40% of votes with a 10%-point lead with the second candidate. The implications of the election are profound for Argentina’s economic prospects.

According to a Poll conducted by CEOP Latam, a market research firm, when voters were asked what their greatest concerns were about the new election, 82.2 percent of the respondents chose “the economy and inflation” as the major concern for the current elections. Indeed, October’s Inflation rate hit 138.30%, the highest inflation rate since 1991, and with the central bank publishing forecast for inflation to reach 169.3%, the situation is more likely to get worse before showing signs of improvement.

Meanwhile, the ruling Peronist coalition has tried to boost its electoral chances by announcing that it will give two payments to informal workers, representing around half of Argentina’s labor force, totaling about 270$. The payouts will be financed by imposing extraordinary taxes on banks and on other big corporation who benefitted the most from the devaluation of peso in august, a measure that was part of the 44-billion financing program for the country made by the International Monetary Fund. This measure was implemented after the Mandatory Open Primaries election result, with the central bank rising the interest rate from 97 percent to 118 percent to weaken the currency to 350 Argentine pesos per dollar.

Currently leading the Runoff that will take the electors to cast their final vote on the 19th of November are Javier Milei, a libertarian from the Liberty Advances Coalition and Sergio Massa, National deputy for the centre-left coalition “Frente de Todos”

The most notable measure in Milei’s plan is to abandon the peso, shutdown the central bank and adopt the dollar as Argentina’s national currency. This maneuver was proposed with the argument that there is no price stability, and the independence of the central bank is just an illusion. Some citizens have already been preparing for a dollarization scenario by trying to acquire as much of the US currency as possible.

One of the main problems faced by Argentina is in fact the currency muddle caused by a multitude of dollar exchange. The government keeps control over the value of the currency by preventing the purchase of foreign exchange to protect its decreasing reserve. The Over-protecting behavior has led to the rise of an informal market for the dollar such that the parallel currency is now at three times the value of the official rate. This disparity has led the way for lots of alternative exchanges, such as the “Coldplay Dollar” for concert tickets or “Soy Dollar” for the agriculture sector.

Argentines convert their cash to dollars on the black market, and the Central bank estimates about 244$ billion is stashed away in homes, which is the ultimate signal of distrust in the peso.

Debt restructuring

Sovereign debt was also a longstanding challenge for Argentina’s governments. In 2022, Argentinian President Alberto Fernandez managed to secure a deal with the International Monetary Fund to restructure $44.5 billion of debt from a 2018 bailout.

In Fact, since 2001 Argentina has defaulted on its international sovereign debt three times.

During the same period, Argentina has gone through two debt restructurings, and from those applied two lessons: the collective auction clauses in the indenture bonds and taking a faster approach into restructuring process.

In the 2020 debt restructuring, Argentina first adopted two controversial measures and then changed actions to complete the restructuring of the desired amount.

These two measures were the “re-designation” and the “pac-man” strategies.

The first would allow the issuer (Argentina) to re-define the pool of bond to be considered for aggregation purposes with the consent of the bondholders. The second instead, would aggregate bonds of various round of the restructuring offering slightly improved terms in each round, to reach a majority of over 75%, allowing Argentina to use a modification method under CAC (Collective Action Clauses) to bind dissenting investors.

These measures have indeed feared investors that thought that this could mean Argentina would be relying on a minority of its creditors to restructure a majority.

Ultimately, Argentina chose not to implement the two measures.

This behavior has allowed the country to avoid a crisis that could have looked similar to the one that happened in 2022.ù

Sovereign debt was also a longstanding challenge for Argentina’s governments. In 2022, Argentinian President Alberto Fernandez managed to secure a deal with the International Monetary Fund to restructure $44.5 billion of debt from a 2018 bailout.

In Fact, since 2001 Argentina has defaulted on its international sovereign debt three times.

During the same period, Argentina has gone through two debt restructurings, and from those applied two lessons: the collective auction clauses in the indenture bonds and taking a faster approach into restructuring process.

In the 2020 debt restructuring, Argentina first adopted two controversial measures and then changed actions to complete the restructuring of the desired amount.

These two measures were the “re-designation” and the “pac-man” strategies.

The first would allow the issuer (Argentina) to re-define the pool of bond to be considered for aggregation purposes with the consent of the bondholders. The second instead, would aggregate bonds of various round of the restructuring offering slightly improved terms in each round, to reach a majority of over 75%, allowing Argentina to use a modification method under CAC (Collective Action Clauses) to bind dissenting investors.

These measures have indeed feared investors that thought that this could mean Argentina would be relying on a minority of its creditors to restructure a majority.

Ultimately, Argentina chose not to implement the two measures.

This behavior has allowed the country to avoid a crisis that could have looked similar to the one that happened in 2022.ù

Consequences of elections on the market

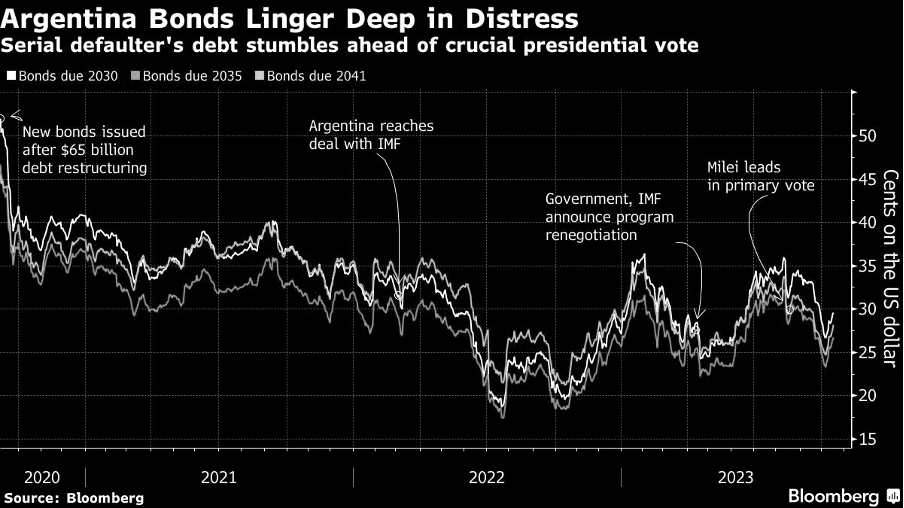

A month ago, anxiety was rising among holders of Argentina’s $65 billion in sovereign bonds before the Presidential Election on the 22 of October, with almost every scenario suggesting further investment losses.

The victory of Javier Milei could have made the dollarization plan become a reality.

The uncertainty in the investors is understandable: Argentina is on the verge of the sixth recession in a decade, while the country’s bond due 2030 have already given losses of 40% since issuance was held during the debt restructuring of 2020. That’s compared with a loss of just 18% in the Latin America sovereign bonds.

A month ago, anxiety was rising among holders of Argentina’s $65 billion in sovereign bonds before the Presidential Election on the 22 of October, with almost every scenario suggesting further investment losses.

The victory of Javier Milei could have made the dollarization plan become a reality.

The uncertainty in the investors is understandable: Argentina is on the verge of the sixth recession in a decade, while the country’s bond due 2030 have already given losses of 40% since issuance was held during the debt restructuring of 2020. That’s compared with a loss of just 18% in the Latin America sovereign bonds.

One month ago, ahead of the elections on 22 of October indeed, there were 3 potential scenarios:

The first one, that saw Milei as a winner, predicted that bond price could have spiked downwards because of its proposal on dollarization, that many economists said would have brought short term inflation even further.

The second one instead, saw Bonds going up in value if Bullrich, former security minister, performed well in the Elections. She indeed gave promises about cutting public spending and diminishing peso printing to cover government bills in the past.

The third one was based on the possibility that Milei faced Massa in November runoff, and the prediction in that case, was an even further decrease in value of bonds, because of his money-printing habits that financed past years spending programs.

At the current state of the Election, the last scenario is exactly where we find ourselves at, the same scenario that investors had feared most. These results represent a reversal of Fortune for Massa, whose coalition had placed third in August primaries.

The day after the election, the country’s overseas notes were among the world’s worst performers, with most falling 2 to 3 cents and benchmark securities due in 2035 dropped below 25 cents on the dollar. This is because, while investors had expected Milei to reach a runoff, Massa’s strong performance had a negative impact on assets valuation because the only market-friendly candidate Patricia Bullrich is out of the race.

Markets are disappointed with the outcome of elections, becauseelections because investors have seen it as a continuation of the policies which have brought Argentina where it is right now.

The first one, that saw Milei as a winner, predicted that bond price could have spiked downwards because of its proposal on dollarization, that many economists said would have brought short term inflation even further.

The second one instead, saw Bonds going up in value if Bullrich, former security minister, performed well in the Elections. She indeed gave promises about cutting public spending and diminishing peso printing to cover government bills in the past.

The third one was based on the possibility that Milei faced Massa in November runoff, and the prediction in that case, was an even further decrease in value of bonds, because of his money-printing habits that financed past years spending programs.

At the current state of the Election, the last scenario is exactly where we find ourselves at, the same scenario that investors had feared most. These results represent a reversal of Fortune for Massa, whose coalition had placed third in August primaries.

The day after the election, the country’s overseas notes were among the world’s worst performers, with most falling 2 to 3 cents and benchmark securities due in 2035 dropped below 25 cents on the dollar. This is because, while investors had expected Milei to reach a runoff, Massa’s strong performance had a negative impact on assets valuation because the only market-friendly candidate Patricia Bullrich is out of the race.

Markets are disappointed with the outcome of elections, becauseelections because investors have seen it as a continuation of the policies which have brought Argentina where it is right now.

Hedge funds bet against Argentina’s bonds

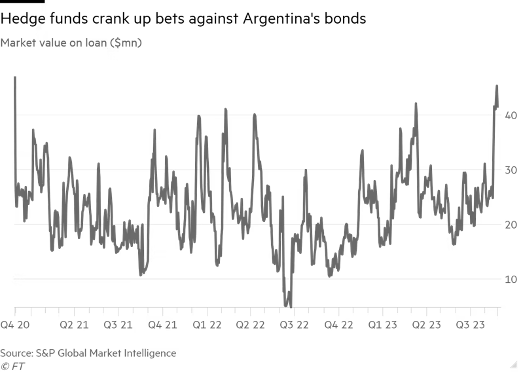

Clear feedback of the economic uncertainty has been shown from multiple Hedge funds, that have started to bet against Argentina’s bonds. The value of Argentina’s bond borrowed by investors to capitalize on a fall in prices has gone up by 65% since Milei won the primary poll ahead of presidential elections. The value of short position against Argentine bonds lent by international custodian banks is currently sitting at $42mln, a steep increase from the $25mln ahead of mid-august vote.

Clear feedback of the economic uncertainty has been shown from multiple Hedge funds, that have started to bet against Argentina’s bonds. The value of Argentina’s bond borrowed by investors to capitalize on a fall in prices has gone up by 65% since Milei won the primary poll ahead of presidential elections. The value of short position against Argentine bonds lent by international custodian banks is currently sitting at $42mln, a steep increase from the $25mln ahead of mid-august vote.

What investors are worried about is the difficulty Milei could be facing in implementing essential reform policies without a majority in Congress, as well as execution risks with Milei, a radical and unexperienced leader.

The price of Argentinas bonds fell as much as 15 per cent after Milei won more than 30 percent of the votes held on August 13.

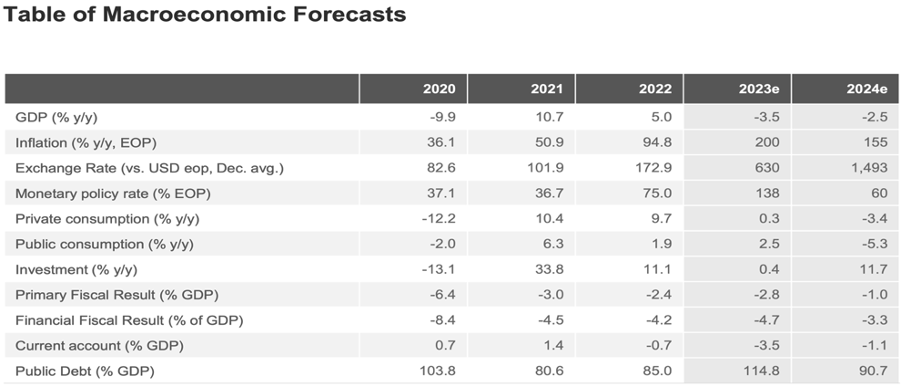

Argentina is currently under a number ofseveral interior and exterior pressures. It has a decreasing GDP, which is expected to contract by 3.5% in 2023 and by 2.5% in 2024. Furthermore, the macro indicators that were hit the hardest in 2023, were gross fixed capital formation with 6.7% and import of goods and services with 7.9%. On top of this, Argentina is suffering from ‘chronic’ high inflation level. While, by no means did Argentina in the past have low inflation, since 2022 we have seen an accelerated increase in inflation levels. With inflation going from 88% in September 2022 to 138.8% in September 2023. Furthermore, Inflation is expected to reach a peak of 200% in 2023.

The price of Argentinas bonds fell as much as 15 per cent after Milei won more than 30 percent of the votes held on August 13.

Argentina is currently under a number ofseveral interior and exterior pressures. It has a decreasing GDP, which is expected to contract by 3.5% in 2023 and by 2.5% in 2024. Furthermore, the macro indicators that were hit the hardest in 2023, were gross fixed capital formation with 6.7% and import of goods and services with 7.9%. On top of this, Argentina is suffering from ‘chronic’ high inflation level. While, by no means did Argentina in the past have low inflation, since 2022 we have seen an accelerated increase in inflation levels. With inflation going from 88% in September 2022 to 138.8% in September 2023. Furthermore, Inflation is expected to reach a peak of 200% in 2023.

History has shown that, when there is unhappiness among citizens regarding the economy of a country usually that also translates into political unrest. It has also been the case for Argentina, who on the 22th22nd of October had the First Round of their presidential elections. Throughout most of the political campaign inflation has been the most talked about issue. The frontrunner to win the elections is Javier Milei of the Freedom Advances. In orderUnexpectedly, not only was he not able to secure a victory in the first round, hebut he also came second in votes with 29.99% of the voters voting him. Neither of the candidates was able to secure the requirements to win the elections in the first round, as such the top two candidates Sergio Massa and Javier Milei will face off on the 19th of November for the second round of elections. A few days after the first roundfirst-round results, Patricia Bulloch, third in the presidential race, publicly shared her support for Javier Milei, Itit remains to be seen if this support, will be enough to close the gap between Javier Milei and Sergio Massa.

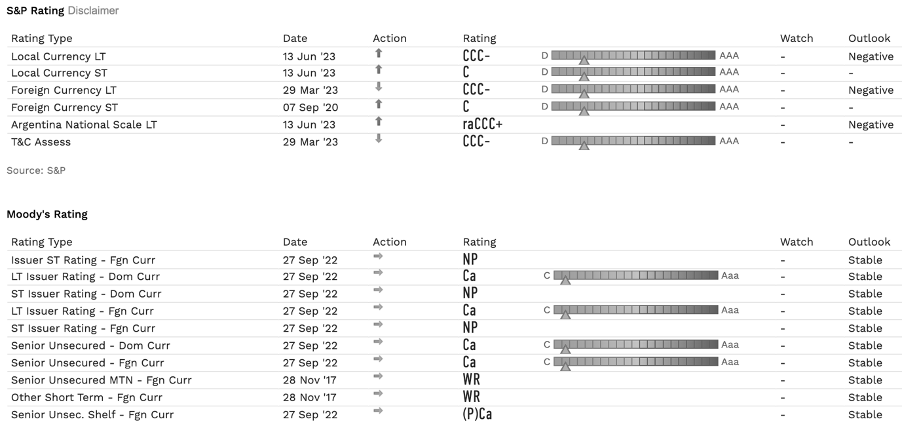

Political and economic uncertainty has an adverse effect on a country’s investor outlook. In recent years Argentina’s Bonds have been downgraded with both their Local Currency and Dollar denominated bonds being rated CCC- by S&P and Ca by Moody’s, both non-prime ratings. On top of this, S&P has a negative outlook on Argentinian debt, certainly affected by the uncertainty that the first round of elections created. On top of this after the first round of elections we saw an increasing number of investors deciding to sell their bonds, which lowered their price. To be more exact the bond that fell the most after the election was the 2035 overseas note falling by 2.3 cents, currently being traded at 23.7 cents. While the average, bond price decrease was between 1.64- 2.16 cents. Important to note, here is that what is interesting is that Argentina has a really highhigh amount of debt with maturity in 2024, putting even more pressure in the Latin American country next year. Furthermore, Argentina has an implied probability of default around 17.18%, this is also reflected on the spread between the short term and long-term bonds, which has lowered significantly in recent years showing the uncertainty that this country has.

On top of this, Argentina and its next President must make a statement, who will they support America and its western allies or Russia and its eastern allies. At the momentNow, Argentina has been offered a spot in BRICS, China’s, and Russia’s new economic alliance, while at the same time Javier Milei, potential future president of Argentina wants to change the country’s currency from Argentinian peso into dollar. While,While we can try to predict Argentina’s future outlookoutlook, it seems almost impossible to be accurate, when the countries facesface both short term and long termlong-term uncertainties. With that being said, after the second round of elections on the 19th of November, we will start to get a better understanding on how the country will be positioned politically for the next 4 years.

By Domenico Destito, Ettore Marku, Giulio Losano

SOURCES

- Federal Reserve

- Financial Times

- European Parliament Think Tank

- International Monetary Fund - World Economic Outlook for October 2023

- Morningstar - Information on rising bond yields

- Reuters - Argentina-China currency swap deal

- Bloomberg